Akash Natarajan and Ananya Viswanathan, a young power couple in their mid-thirties. Akash’s days are consumed by performing heart surgeries in the operation theatre. Meanwhile, Ananya spends her time preparing arguments for her legal cases. Their careers are taking off and while they’ve already tasted success, they know the best is yet to come. Their children recently started going to school. For the last 8 years, home for Akash and Ananya was a small rented 3BHK flat in Pune.

With promising careers ahead of them, they begin contemplating buying a house of their own.

| Salary drawn by Akash | ₹ 2,00,000 |

| Salary drawn by Ananya | ₹ 1,25,000 |

| Total Monthly Inflows | ₹ 3,25,000 |

| Monthly Household Expenses | ₹ 1,25,000 |

| Loan EMI – Vehicle | ₹ 40,000 |

| Savings | ₹ 1,60,000 |

First Time Real Estate Investor

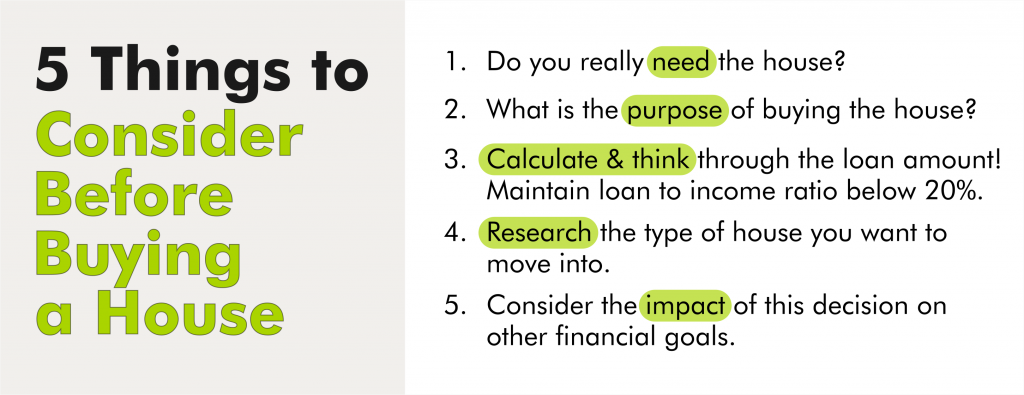

Akash and Ananya were both nervous and excited about making this big decision. So much rested on getting it right. Central location, fair price, and an upscale location were key. They wanted to make the right choice for their children – a neighbourhood that was a good environment for them to grow up in.

Before making a big decision like buying a house, everyone should contemplate a few questions:

Here is a quiz that can help you evaluate whether you are ready to buy a house!

Rental Property for Sale

Ananya spotted the perfect luxury residency project in Pune for them to live in. Akash was keen to buy an apartment in the project. On the other hand, Ananya feels that renting is a better option for their family.

Buying property

The current value of the house is ₹ 1 Crore. Akash does the math behind buying this house. He has ₹ 20 Lakhs in hand and would have to borrow the rest. After talking to his bank, he settles on a home loan of ₹ 80 Lakhs at an interest rate of 7% for 20 years.

| Cost of the house | ₹ 1,00,00,000 |

| Down payment – 20% | ₹ 20,00,000 |

| Home loan – 80% | ₹ 80,00,000 |

| Stamp Duty – 3% of property value | ₹ 3,00,000 |

| Interior decoration, furnishing | ₹ 10,00,000 |

| Total investment | ₹ 1,13,00,000 |

Akash had not factored in the cost of incidental charges in his calculations. He was quite shocked to realize that it totalled 13% of the original cost. He would finance the incidentals by dipping into his emergency fund and breaking a long-term fixed deposit.

Real Estate Investment Vs Mutual Funds India

Ananya was not convinced that the apartment was a good investment. She had read that property prices in that area had grown at 5%-7% in the last ten years. With a surplus of new apartments coming up in the locality, she wasn’t sure the market would evolve favourably. So, she decided to compare this investment in real estate versus mutual funds.

Return on Investment

| Value of the property after 15 years @ 6% | ₹ 2,70,00,000 |

| Maintenance cost for 15 years | ₹ 15,00,000 |

| Property taxes @ ₹ 50,000 p.a. | ₹ 7,50,000 |

| Brokerage fees and expenses @ 5% | ₹ 13,50,000 |

| Value of Property | ₹ 2,34,00,000 |

| Less Interest Paid on Home Loan | ₹ 49,50,000 |

| Less Cost of Property | ₹ 1,13,00,000 |

| Net Gains | ₹ 71,50,000 |

Ananya calculated a net gain of ₹ 71.5 Lakhs over 15 years.

Scope for higher returns

Ananya thought that mutual funds could deliver better returns than real estate.

The down payment for the house is ₹ 20 Lakhs. If Akash agreed to stay on rent, he can invest this money in a mutual fund portfolio that grows at 8%-10% CAGR. Their home loan EMI works out to ₹ 72,000 for 15 years, whereas the rental costs are ₹ 45,000. The difference could be invested as a SIP.

| Cash in Hand | ₹ 20,00,000 |

| Monthly Investments | ₹ 27,000 |

| Total amount invested in 15 years | ₹ 68,00,000 |

| Portfolio value after 15 years assuming 8% CAGR | ₹ 1,72,00,000 |

| Net Gains | ₹ 1,04,00,000 |

The math showed that mutual funds were a better investment. However, Akash insisted that owning mutual funds didn’t give them the same satisfaction as owning a house. Some things couldn’t be captured in terms of financial values.

Advantages of Renting a Property

Ananya believed renting was a better option for the following reasons:

-

-

- Flexibility – they wouldn’t be tied down to Pune as their careers progressed.

- Career breaks can be taken without worrying about EMI.

- Cost – Incidental costs in acquiring Property – Stamp duty, Property tax, etc can be avoided. The owner will be responsible for the maintenance and repair costs.

- Financial Savings – Buying a house takes away liquidity and adds to liability. By renting they create more liquidity and are able to construct a wealth corpus.

-

Buying Vs Renting: What Is better?

Ananya and Akash realised that personal, financial, and emotional factors played a crucial role in the buying vs renting decision. Ananya’s reasons to rent stemmed from a place of seeking financial security. Akash’s reasons to buy arose from an aspiration to be a homeowner.

Buying vs renting is based on being able to afford the down payment, closing costs, along with ongoing costs associated with maintaining a home.

| Buying | Renting | |

| Asset Creation | Invest in real estate which can be illiquid but creates wealth over time. Real estate investments are also assets that you can use. | Flexible to create a diverse and liquid portfolio across instruments like stocks, bonds, mutual funds, and ETFs. |

| Residence | Homeowner, even if you buy the house on a loan. | May be forced to change residences based on lease agreements and homeowner’s needs. |

| Benefits | Buying gives stability and pride of ownership | Renting offers flexibility and easy mobility. |

| Tax Implications | Tax benefits under Section 80 C, 80EE ,24 | House Rent Allowance |

Pros and Cons of Real Estate Investing

Advantages of Real Estate Investing

-

-

- Long term capital appreciation.

- Regular cashflows through rental income.

- Diversification: Real estate as an asset is not directly correlated to the stock market.

- Inflation hedge: Rental yields and real estate prices tend to increase in an inflationary environment.

- Tax benefits under Sections 24, 80 C, 80 EE.

-

Disadvantages of real estate investment

-

-

- High capital requirement

- High transaction costs: Buying and selling real estate is costly and time-consuming. Professionals like appraisers, lawyers, real estate agents, financial advisers, and tax consultants may need to be involved.

- Depreciation: Buildings can lose value over time due to use, newer projects, real estate market cycles, or development of other neighbourhoods.

- Illiquidity: Real estate properties are relatively illiquid. It might take months or even years, to sell the property at a fair price.

-

Tax Implications

Akash felt that another point in his favour, were the associated tax benefits.

Section- 80C

A tax deduction of up to ₹1.5 lakh per financial year can be claimed for the principal paid. This may include stamp duty and registration charges as well, but that can be claimed only once.

Section – 24

Deductions of up to ₹2 lakh on the interest amount can be claimed under Sec 24 of Income tax act. These deductions apply only on the property whose construction is completed within five years. If construction is not completed within this time frame, you can claim only up to ₹30,000. This deduction can be claimed every financial year.

Section – 80EE

First-time homebuyers can claim an additional ₹ 50,000 on the interest amount every financial year.

-

-

- Loan amount must not be more than ₹ 35 lakh.

- The property’s value must be within ₹ 50 lakh.

-

Choosing a Home Loan

Akash spent some time studying home loans. He knew they wouldn’t be able to finance the property entirely through their savings.

Home Loan Interest Rates

First, he learnt that home loan interest rates could vary because of the following reasons:

-

-

- Fixed vs Floating Rate

- Benchmark used – MCLR vs RLLR

- Secured vs Unsecured loans

- Borrower’s credit score

- Term of Loan

-

What is better? Fixed or Floating Rate Loan?

| Fixed Rate of Interest | Floating Rate Interest | |

| Interest Rate | Fixed for the term of the loan | Floating component linked to a benchmark |

| Partial Prepayment | Charges are applicable per home loan agreement | No charges |

| Premature closure | Charges are applicable per home loan agreement | No charges |

When interest rates are low, locking into a fixed interest loan is a good idea. This ensures that your cost of borrowing remains low through the term of your home loan. If interest rates are high, a floating rate loan allows you to reduce your cost of borrowing as the interest rate cycle turns.

How Much Should You Borrow For Your First House?

Ananya and Akash were unable to settle the debate between themselves. Ananya felt uncomfortable taking a huge home loan when they had so many financial commitments in the coming years. Akash was convinced that the future meant more money. What seems like a huge home loan today, would be easily affordable a few years down the line. Besides, if she was so worried about the huge EMI, they could simply extend the loan.

So, they analysed the numbers with their financial planner.

Down Payment

Ananya was right, the more you put down initially, the lower your EMI becomes.

| Value of house | ₹ 1,00,00,000 | ₹ 1,00,00,000 | ₹ 1,00,00,000 |

| Down Payment | 20% | 40% | 60% |

| ₹ 20,00,000 | ₹ 40,00,000 | ₹ 60,00,000 | |

| Loan | 80% | 60% | 40% |

| ₹ 80,00,000 | ₹ 60,00,000 | ₹ 40,00,000 | |

| Interest rate | 7% | 7% | 7% |

| Term of Loan | 15 years | 15 years | 15 years |

| Loan EMI | 71,906 | 53,930 | 35,953 |

| Total Amount paid to bank | ₹ 1,29,43,127 | ₹ 97,07,345 | ₹ 64,71,564 |

| Interest paid to bank | ₹ 49,43,127 | ₹ 37,07,345 | ₹ 24,71,564 |

| Principal repayment | ₹ 80,00,000 | ₹ 60,00,000 | ₹ 40,00,000 |

Tenure of the loan

Surprisingly, Akash was right too! You can reduce your EMI by increasing the term of your loan.

| Particulars | Scenario 1 | Scenario 2 | Scenario 3 |

| Value of house | ₹ 1,00,00,000 | ₹ 1,00,00,000 | ₹ 1,00,00,000 |

| Down Payment | 20% | 20% | 20% |

| ₹ 20,00,000 | ₹ 20,00,000 | ₹ 20,00,000 | |

| Loan | 80% | 80% | 80% |

| ₹ 80,00,000 | ₹ 80,00,000 | ₹ 80,00,000 | |

| Interest rate | 7% | 7% | 7% |

| Term of Loan | 10 years | 15 years | 20 years |

| Loan EMI | ₹ 92,887 | ₹ 71,906 | ₹ 62,024 |

| Total Amount paid to bank | ₹ 1,11,46,414 | ₹ 1,29,43,127 | ₹ 1,48,85,740 |

| Interest paid to bank | ₹ 31,46,414 | ₹ 49,43,127 | ₹ 68,85,740 |

| Interest paid as % of value of house | 31% | 49% | 68% |

Akash pushed for Scenario 3 because it feels like he was paying less. It also meant they could own a house today instead of five years down the line. However, once you factor in how much interest is paid over the term of the loan, you realize that the cost of the house increases by 68%.

Buying Property now or later?

Akash and Ananya concluded that the best way to make this decision would involve their financial planner. After taking into consideration Akash’s aspirations and Ananya’s worries, their financial planner suggested that they wait for a few years before buying a house. Their financial planner explained her recommendation based on the following reasons:

-

-

- Financial Stability

- Interest Cost & Loan to income ratio

- Risk Management

- Financial Priorities

-

Financial Stability

Akash was optimistic about their career growth, but this is not something one takes for granted. Banking on future income to pay off a home loan was not a financially stable strategy. However, if they were patient and waited a few years, they could capitalize on their income growth to save more and plan their EMI outflows. Their financial planner explained that while this seemed like a once in a lifetime opportunity, there would be plenty in the future. They would have no regrets if they let this slip by.

Financial Risk Management

Akash planned to drawdown from his emergency fund to finance the incidental costs. EMIs only added to their monthly commitments. Moreover, their household expenses would increase. Going forward they would be responsible for maintenance and repairs and they must increase their life insurance premiums.

Depleting the emergency fund was not even an option. In fact, there were compelling reasons to top it up.

Interest Cost & Loan To Income Ratio

Akash was worried that home loan interest rates would rise in the next few years. Their financial planner pointed out that now they could afford home loans that ran for 15-20 years. By waiting a few years, they would be able to reduce the term of their home loan by at least 5 years. Overall, they would not lose money by delaying the decision.

In the best-case scenario, their loan to income ratio was above 20%. Ideally, with two young children in the family, their loan to income ratio should remain below 20%.

Financial priorities

Ananya’s financial priority was to provide for their children’s school and college education. She was sure she wanted to send them abroad and had expected to spend at least ₹ 1 Crore on each child. Owning a house came after that. Akash believed they could achieve both comfortably, even if it didn’t seem that way at the moment.

Their financial planner projected their cash flows for the next few years. Even assuming Ananya earned a decent bonus and Akash saw phenomenal career growth, they would need to stretch their savings. Saving up for their children’s higher education abroad was significantly more expensive than they had projected. They had to factor in inflation, currency depreciation, and living costs. Cutting back on their lifestyle seemed like an unnecessary measure for a family that was doing well financially.

Ultimately, buying a house too soon would mean that Akash and Ananya would spend more time worrying about the decision than enjoying the achievement of being homeowners.