Retirement planning is not about building the perfect plan. It is about building a plan that survives imperfection. Markets deliver surprises. Inflation has moods. Retirement planning in India has historically relied heavily on fixed-income options such as deposits and provident funds, which often fall short in effectively mitigating inflation and increasing life expectancy risks.

The process of stress testing your retirement corpus is a structured exercise that asks: “What does our plan look like when things go differently from what you assumed?” Think of it as crash-testing a car. You hope you never need the safety features. But you absolutely want them there.

Three stress test scenarios every retirement corpus must pass- before life does the testing for you.

Stress Test 01

What If Your Returns Never Arrive as Planned?

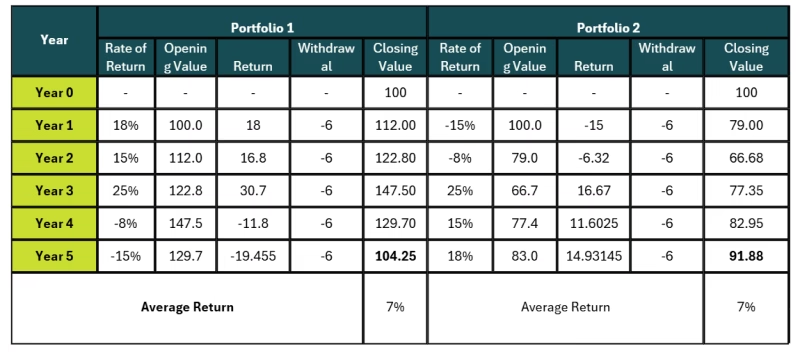

Every retirement plan begins with an assumed rate of return. You budget for 10% or 12% per annum from equity, 7% from debt, and blend them into a comfortable blended return of, say, 9%. The plan looks robust. But what if markets deliver 6% for the first five years of your retirement?

The Sequence-of-Returns Trap

Poor returns in the early years of retirement are disproportionately damaging.

From the above analysis we can infer that even if the portfolios have the same set of returns over the years, the sequence of returns is what affects the income which further affects the average return. A lower return in initial years in portfolio 2 can cut your retirement runway for some years. The smarter way to address this risk is to use rental income or other steady inflows alongside the SWP strategy. These cash flows act as a natural income buffer, reducing the need to withdraw from investments during market downturns and improving the long-term sustainability of the retirement corpus.

Stress Test 02

What If Inflation Refuses to Behave?

India’s CPI has averaged around 6% over the last decade, but personal inflation – the inflation that hits your specific lifestyle – often runs higher. Healthcare inflation in India runs at 12–14% per annum. If you are 60 today and your medical expenses are ₹1.2L a year, they could be ₹10L+ a year by the time you are 80. Your plan budgeted for 6%. Reality may consider 9%-10%. Even a small underestimation of inflation can have a huge impact over long retirement periods because inflation compounds every year.

The structural answer to inflation is maintaining meaningful equity allocation even post-retirement , typically 40–50% for a 60-year-old ,so that the growth engine in your portfolio keeps pace with the purchasing-power erosion in your withdrawal bucket. Another practical safeguard is creating a separate healthcare corpus dedicated exclusively to future medical expenses. Since healthcare inflation often rises much faster than general inflation, isolating these costs from the core retirement portfolio reduces the risk of medical shocks derailing long-term income sustainability.

Must Read: The Hidden Risk of Having Most of Your Wealth in ESOPs

Stress Test 03

Have you considered longevity into your plan? What If You Need Long-Term Care?

This is one of the most overlooked retirement risks and potentially one of the most financially disruptive. Long-term care becomes necessary when chronic illness, cognitive decline, or physical disability makes independent living difficult over extended periods. Conditions such as dementia, Parkinson’s disease, stroke recovery, and prolonged cancer treatment can require sustained professional support, with costs ranging from ₹60,000 to over ₹2–3 lakh per month depending on the level of care, city, and medical complexity often continuing for several years. One major reason to plan for longevity is the increased likelihood of needing long-term medical care later in life. Living longer means retirement savings must last for more years, but it also raises the possibility of higher healthcare expenses, ongoing medical support, and assistance with daily living needs. Unlike short-term medical emergencies, long-term care creates recurring cash-flow pressure that can quietly erode even a well-funded retirement corpus. The biggest threat to retirement is often not a market crash but a health event that turns into a monthly financial obligation for years.

A three-year care requirement at ₹1.5 lakh per month can introduce a massive unplanned cash-flow burden into even a well-designed retirement plan. Without a dedicated provision Plus underestimated distribution period, may forced retirees to liquidate investments during vulnerable years, permanently weakening the sustainability of the corpus.

Longevity is also systematically underestimated, because people anchor to average life expectancy rather than their individual probability of reaching advanced age. If you are healthy, non-smoking, and from a family with longevity, your plan should run to 85- 90.

The answer to longevity risk is to build retirement plans with a wider safety margin – not for age 80, but potentially for age 85 or above with a separate corpus to fund long term care. This means combining growth assets like equity for long-term inflation protection, stable income sources such as pensions or rental cash flows, and flexible withdrawal strategies that can adapt over time. Plan for at least 30 years of retirement, factoring in potential early losses. It is also important to work with a financial expert to estimate a realistic retirement distribution period based on your health profile, family longevity history, and lifestyle factors.

Long-term care planning is therefore not just a financial exercise, but a family-level decision. Conversations around who will provide care, how expenses will be funded, and what insurance or support structures are available should ideally happen in the late 50s or early 60s – not in the middle of a medical crisis at 78.

“The goal of a stress test is to give you the gift of time – time to fix what is fragile, before fragility becomes failure.”

What a Stress-Tested Plan Actually Looks Like

A retirement plan that has been stress-tested is not just a projection with a happy ending. It is a system with multiple layers of resilience – a liquidity buffer for bad market years, a separate healthcare reserve for medical inflation, an equity allocation that funds longevity, and a long-term care provision that protects everything else.

It is also a plan that has been reviewed by an advisor who asked the uncomfortable questions – not to dampen your optimism, but to stress-test it against reality and return it to you stronger.

Most people do this work once, at retirement. The right time to stress-test is 7–10 years before retirement – when you still have time, earning capacity, and compounding on your side to course-correct.

Don’t Just Plan for Retirement. Invest for It.

A retirement plan is only as strong as the investments supporting it. While projections may look comforting on paper, real-life retirement is shaped by market cycles, inflation, rising healthcare costs, and the possibility of living longer than expected.

The key is not to build a plan based on perfect assumptions, but to invest in a portfolio designed to adapt, endure, and grow through uncertainty. A well-structured investment strategy can help create the resilience needed to sustain income, preserve purchasing power, and support your lifestyle throughout retirement.

At ithought, we combine comprehensive financial planning with ongoing portfolio monitoring, asset allocation reviews, and research-backed insights to help build resilience into your retirement journey.

Invest with us and let our actively managed, research-driven investment approach help you build a retirement portfolio that is not just designed for the future- but prepared for it.