India is entering the current phase of geopolitical uncertainty — including the emerging Iran war–related energy and trade disruptions — from a relatively stronger domestic footing. While the conflict has already pushed up crude prices and introduced volatility in currency and capital flows, the domestic demand environment is showing early signs of stabilization, supported by improving household balance sheets, stronger real credit growth and resilient employment trends in key urban sectors.

Household leverage and credit trends

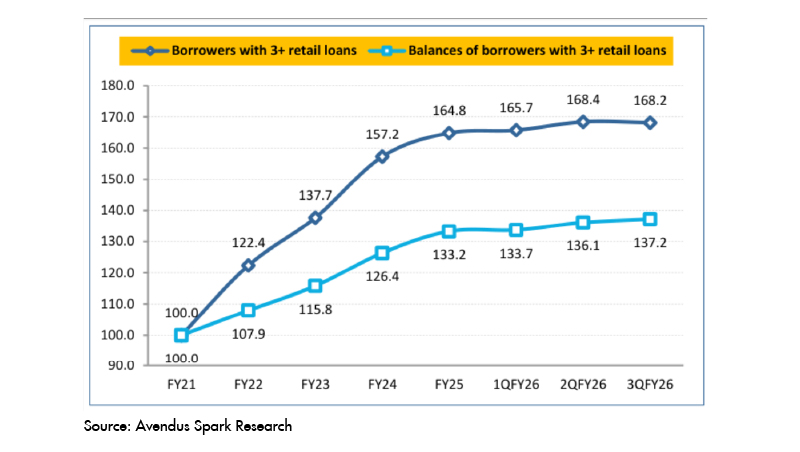

The worst phase of household balance-sheet stress appears to be behind us. Growth in multi-loan borrowers has plateaued and there is visible deleveraging underway in unsecured retail segments.

Additionally, improvement in the FOIR (EMI-to-income ratio) over the past 6–9 months, pointing to gradual normalization in household financial health.

Supporting this, real credit growth has accelerated meaningfully. Adjusted for CPI inflation, real credit growth improved from 6.4% in March 2025 to 12.2% in January 2026, indicating a rebound in economic activity and consumption demand.

Urban consumption – hiring dynamics remain the key driver

Urban consumption continues to be closely linked to employment and salary growth, particularly in technology and services sectors.

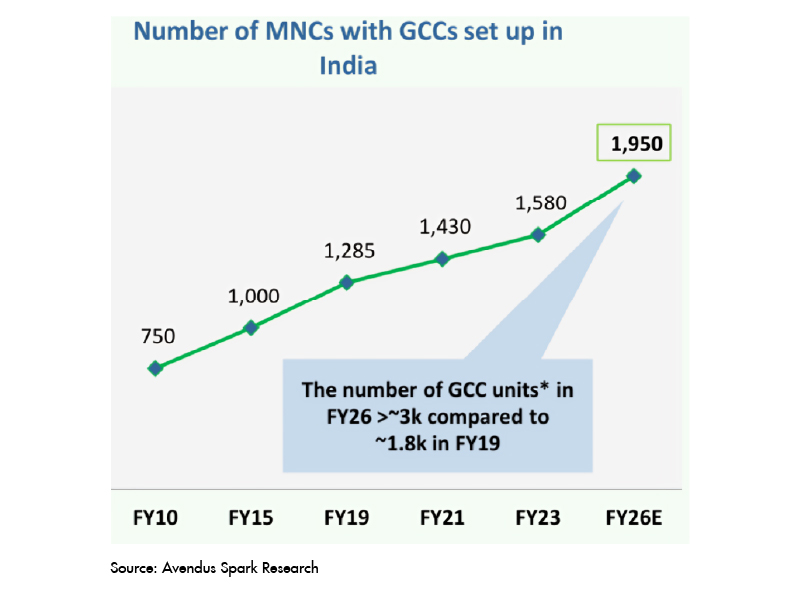

As per the data from Avendus Spark, Hiring momentum in technology sector is increasingly shifting toward Global Capability Centers (GCCs), which are expanding faster than traditional IT services firms. In FY25, salary costs for listed IT services companies grew only ~4%, whereas Tier-1 and other GCCs saw ~12–13% growth, highlighting stronger hiring momentum in these organizations.

Talent absorption patterns are also shifting. Only 20–25% of STEM graduates are entering IT services today versus ~65% historically, while GCCs are absorbing ~40–45%, partially offsetting the slowdown in IT/ITES hiring.

Across sectors, hiring activity grew 7.4% during 11M FY26, led by Defence/Government, Travel, BPO, Real Estate and Media.

Employee costs for companies with market cap > ₹10bn increased ~12% YoY in Q3 FY26, indicating improving wage momentum. Incremental hiring remains healthy across product companies, fintech, BFSI analytics teams, e-commerce and manufacturing, while entry-level IT hiring has stabilized though still below historical peaks.

Rural demand – resilient but weather sensitive

Rural consumption has been supported by higher rural wage growth and lower inflation, sustaining non-farm rural demand momentum. A notable positive has been strong two-wheeler demand, which surged in higher double digits following GST rationalization, signaling recovery in rural discretionary spending.

However, the key risk remains weather. A weak monsoon outlook for 2026 could weigh on farm-linked rural demand. That said, adequate water availability should cushion the downside in the first year of weak rainfall, limiting immediate disruption.

Overall, the sector appears to be transitioning from a phase of balance-sheet stress toward a gradual normalization in demand, placing it in a relatively stronger position to navigate potential headwinds arising from an adverse geopolitical environment.

In a market shaped by shifting global risks and domestic resilience, identifying the right opportunities requires both perspective and discipline. If you are looking to position your portfolio for the next phase of India’s consumption story, we would be glad to partner with you on that journey.