As we closed the books on FY26, the Indian automotive industry has proven its mettle. Despite whispers of production disruptions and demand uncertainty, the sector sustained its growth momentum right through March 2026. This wasn’t just a story of “selling cars”—it was a strategic shift toward premiumization, SUV dominance, and a structural rural recovery fuelled by GST rationalization.

The Scoreboard: Winners and Laggards of FY26

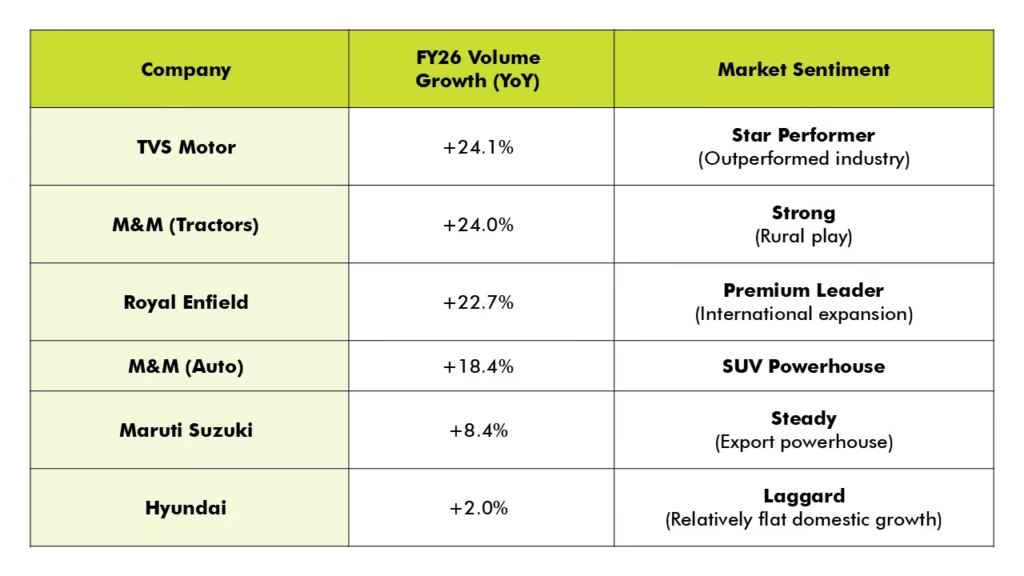

The fiscal year concluded with a robust March, but the real story lies in the Year-to-Date (YTD) performance. We saw a clear divergence between those riding the “premium” wave and those stuck in the slow lane.

Key Themes: What Moved the Needle?

1. PV: The SUV “Goliath” and Premiumization

The Passenger Vehicle (PV) segment was dominated by Utility Vehicles (UVs). Mahindra & Mahindra saw a 25.4% jump in domestic UV volumes in March alone, capitalizing on GST rationalization and new launches. Meanwhile, Tata Motors is doubling down on the “premium” consumer with the launch of the Tata Sierra and the Harrier Petrol version. Even the industry giant, Maruti Suzuki, is finding growth in UVs (up 16.8% in March) with new models like the Victoris.

2. Two-Wheeler Recovery in H2 FY26:

The 2W segment benefited from a set of positive factors: GST rate cuts, new model launches, and the early timing of Chaitra Navratri.

3. Commercial Vehicles:

The CV segment remained a reliable indicator of economic activity. Tata Motors and VECV reported growth driven by mining and construction.

4. Tractor: Tractor OEMs reported strong double digit volume growth performance led by strong rural sentiments and GST cuts.

Strategic Positioning:

We believe the “easy” volume growth is behind us. To win in FY27, investors should look for companies positioned for EV transition and good product launch pipeline over the next 2-3 years.

Translate these market opportunities into action- start investing with us.