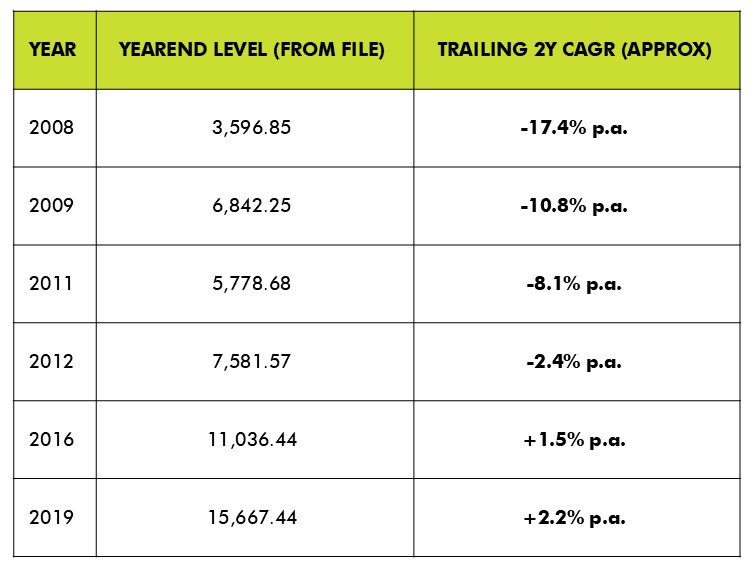

Over the past two decades, the S&P BSE 500 has gone through several periods when even two‑year rolling returns have been in low single digits or negative. These phases can feel like “dead money” for investors and naturally raise questions about whether equities still work over a reasonable holding period.

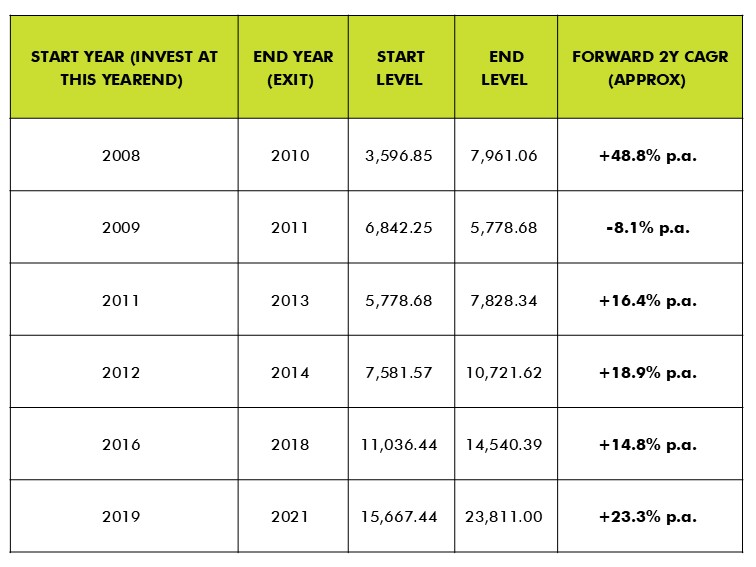

History, however, suggests that such periods have usually been set‑ups rather than end‑states. In multiple episodes where the BSE 500’s trailing 2‑year CAGR dropped below 10% (for example around 2008–09, 2011–12, 2016 and 2019), the subsequent two‑year returns from those points were predominantly strong double‑digit annualised, often in the mid‑teens to high‑teens, and at times much higher. Only one of these “signal” years was followed by a weak next two‑year phase; the rest rewarded investors who stayed invested or added to positions.

The underlying reason is straightforward: extended periods of low or negative returns typically coincide with heightened uncertainty, earnings downgrades and de‑rating. As prices adjust faster than long‑term fundamentals, expected returns from those lower levels tend to rise. When conditions stabilise and earnings recover, markets often move sharply higher, compressing several years of returns into a relatively short window.

The current environment, where rolling two‑year returns have again cooled towards low double digits, is consistent with that historical pattern. While this does not guarantee an immediate rebound, it does argue against extrapolating today’s muted returns into the future. For long‑term investors with a 3–5 year horizon, past cycles suggest that periods of low single‑digit 2‑year returns have more often been an opportunity to stay the course or selectively add, rather than a signal to exit equities.